Building and maintaining target allocations is a critical component of successful wealth management. However, this process becomes increasingly complex when considering the nuanced needs of different family members and the intricate structures often employed in family offices.

Understanding Entity Structures

Family offices often utilize various legal entities to manage and distribute wealth efficiently. Common structures include:

- Trusts: Used for asset protection, tax planning, and controlled distribution of wealth

- Limited Liability Companies (LLCs): Offer liability protection and flexible management structures

- Family Limited Partnerships (FLPs): Facilitate wealth transfer and centralized asset management

Each entity may serve a specific purpose, such as providing for a particular family member's needs, funding education, or supporting philanthropic efforts. Understanding these structures is crucial, as they form the foundation upon which allocation strategies are built.

Aligning Entity Allocations with Family Need

When creating target allocations, it's wise to consider the purpose of each entity and its relationship to family members:

- Trusts for younger generations might focus on long-term growth, while those for older family members may prioritize income generation.

- Entities designated for specific purposes (e.g., education funds) should have allocations that align with their time horizons and objectives.

- Consider creating complementary allocations across entities to achieve overall family goals while meeting individual needs.

Assessing Risk Tolerance

Risk tolerance can vary significantly among family members and across different entities:

- Use comprehensive risk assessment tools that consider both quantitative factors (e.g., time horizon, liquidity needs) and qualitative factors (e.g., personal comfort with volatility).

- Consider hosting family workshops to discuss risk, ensuring all members understand the concepts and their implications.

- Recognize that risk tolerance may differ for various pools of assets. For instance, a family member might be more risk-averse with assets earmarked for their children's education compared to assets for long-term growth.

Incorporating Market Conditions

Market conditions play a crucial role in allocation decisions, but it's important to balance short-term market movements with long-term strategic goals:

- Educate family members on economic indicators and their potential impact on different asset classes.

- Discuss how market cycles might affect various family entities differently based on their time horizons and objectives.

- Consider implementing a systematic review process that allows for tactical adjustments while maintaining strategic allocation targets.

Aligning Allocations with Values and Goals

Family values and long-term goals should be a cornerstone of allocation strategies:

- Facilitate discussions on the family's mission and how it translates to investment philosophies for different entities.

- If important to the family, incorporate ESG (Environmental, Social, Governance) factors into allocation decisions.

- Balance financial objectives with legacy planning and philanthropic goals, potentially creating separate allocations for charitable entities.

Strategies for Family Involvement in Entity-Level Decisions

Engaging family members in the allocation process can lead to better outcomes and smoother wealth transitions:

- Establish a family investment committee to oversee allocation strategies across entities.

- Use role-playing exercises to help family members understand different perspectives on entity allocations.

- Involve younger generations in age-appropriate ways, such as managing a small portion of assets or participating in educational investment games.

- Provide education on fiduciary responsibilities, especially for those who may become trustees or managers of family entities.

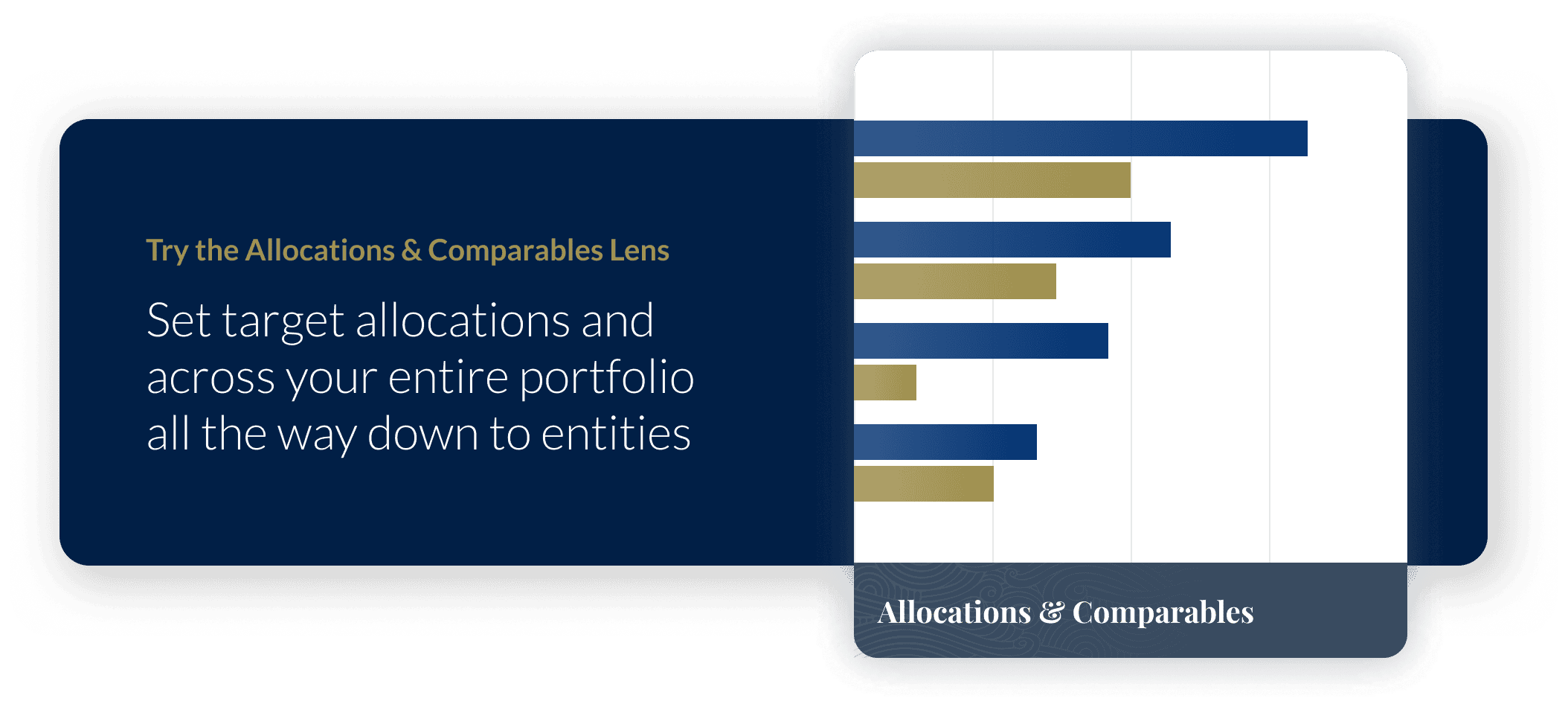

Using Technology to Enhance Family Discussions

Leverage technology to facilitate understanding and decision-making:

- Use allocation visualization tools to illustrate how different scenarios might play out across various family entities.

- Employ the Allocations and Comparables lens to compare entity-level allocations against benchmarks or family-wide targets.

- Utilize virtual meeting platforms and collaborative online tools to ensure all family members can participate in discussions, regardless of location.

Handling Disagreements and Reaching Consensus on Allocations

Disagreements are natural in family settings, especially when it comes to financial decisions:

- Establish clear decision-making protocols for entity-level allocations.

- Consider using a neutral third-party facilitator for particularly contentious discussions.

- Emphasize the importance of compromise and the family's overarching goals.

- Document all decisions and the reasoning behind them to provide clarity and avoid future conflicts.

Regular Review and Adaptation of Entity Allocations

Allocation strategies should evolve with the family and market conditions:

- Set a regular schedule for reviewing entity-level allocations, perhaps quarterly or semi-annually.

- Be prepared to adjust allocations as family circumstances change, such as marriages, births, or new business ventures.

- Use these review sessions as opportunities for ongoing financial education for family members.

Conclusion

Building target allocations in a family office setting requires a delicate balance of financial acumen, family dynamics, and strategic planning. By taking a family-centric approach that considers the unique needs of different entities and family members, you can create a robust allocation strategy that stands the test of time.

Looking for a better way to track your target allocations? Copia can help- get started today.

Less Common Tax Documents You Should be Aware Of

Net Worth: Beyond the Basics